For years, I looked at my LIRA and felt that something was off. The balance was going up, but the gains just didn’t reflect what I was seeing in the market. I couldn’t prove it on my own, so I asked Google Gemini to compare my results with the broader market and other types of funds. Its answer lined up with my gut: my mutual funds weren’t only charging me fees, they were also leaving me with less gains over time.

What made my mutual funds grow much slower

When I left my old job, I wasn’t given many options for where to put my LIRA. I was told I could keep my funds with the fund provider or take them out and pay taxes on them. I obviously left the funds with the fund manager. They had pre-selected funds, and I didn’t know enough to choose individual investments. And life was busy, so I didn’t think much about it at the time. The problem showed up later. I was paying for management, and in many cases I was still getting returns that lagged cheaper options. Over a few months, that gap felt small. Over years, it turned into real money left on the table.

I stayed because for a long time I didn’t know what I was doing. I figured the fund managers and my financial advisors had the knowledge, so why would I go against them. I trusted that a recommended product had already been screened for me. And my account balance usually went up, and no one was calling to say anything was wrong. When I talked to my financial advisor who administered the funds, she assured me that what I was invested in would give me higher returns according to my risk profile.

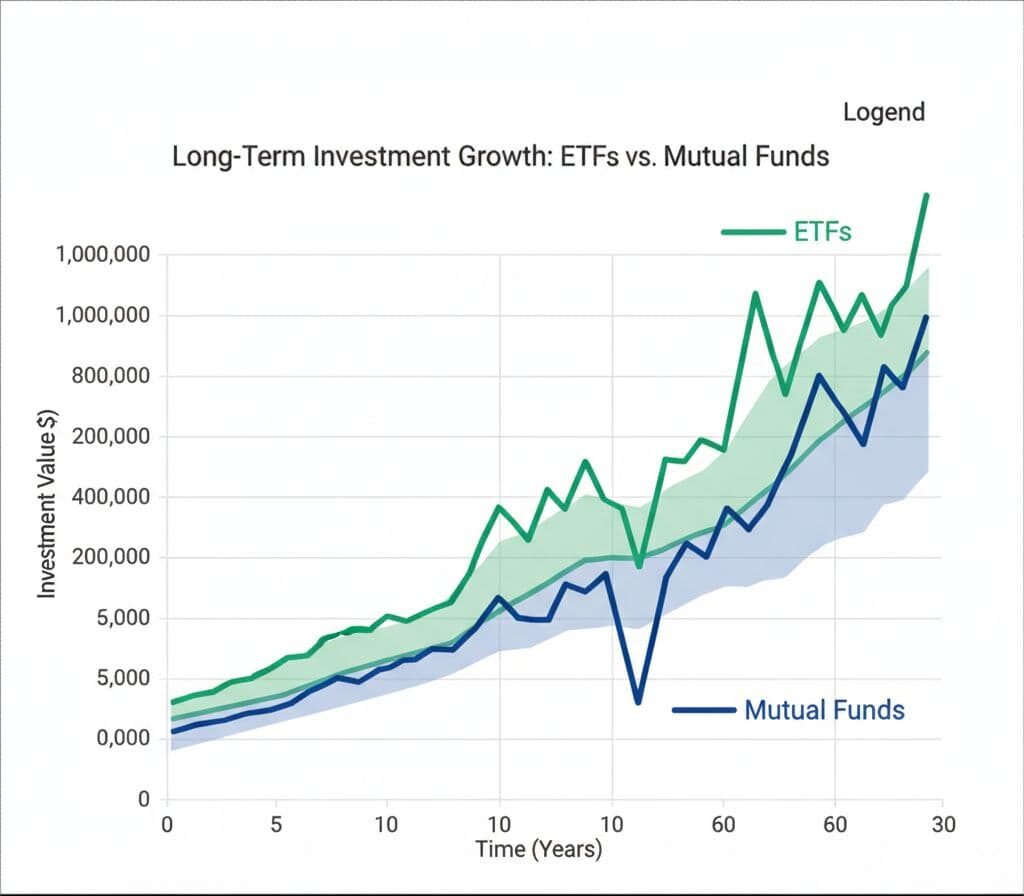

When markets are rising, most mutual funds still show gains. That makes underperformance hard to spot. A fund that earns 4.4% when a lower-cost option earns 8% doesn’t look alarming in one year. After 10 years, that gap can become huge because compounding keeps building on the smaller base.

How fees took money out of my future

The biggest lesson for me was that fees don’t need to look dramatic to do damage. If a fund charges a 2% MER and a broad-market ETF costs 0.2%, that difference comes out of my return every year. Instead, part of my growth was getting shaved off before I ever saw it. I used to focus on the balance, not the cost. That was a mistake.

If two portfolios both track a market with 8% returns. One loses 0.2% to fees, while the other loses 2%. That leaves me with about 7.8% in one account and 6% in the other. That 1.8% gap doesn’t sound big. Yet on $100,000 over many years, it can mean thousands, then tens of thousands, in missed growth.

The 2016 to 2026 bull market made the gap even bigger

The last decade made this easier to see. From 2016 to 2026, markets had long stretches of strong growth. My accounts saw gains, so at first I thought things were fine. But Google Gemini helped me compare my results against broader market performance. That comparison made the lag hard to ignore. A rising balance can make almost any choice look smart. If my account goes from $80,000 to $96,000, I feel progress. But, if a lower-cost portfolio would have reached $102,000 over the same period, I didn’t really keep up.

Compounding works in both directions. It grows gains, but it also grows the lag. If I miss 1% or 2% a year, the shortfall doesn’t stay small. Each year starts from a lower amount, so the gap grows. A LIRA (Locked In Retirement Account) is money that can’t ever be contributed to. So any gains I get are due to the growth of the market. Low returns in a locked-in account feel worse because I have less ability to fix a bad setup with increased contributions. And in a locked-in account, lost time matters.

I gave Gemini the rough history of my account and asked what similar money might have done in a lower-cost, self-directed portfolio. Once I saw how far my returns could have gone with lower fees, the missed gains were clear.

What I would do differently with mutual funds and self-directed investments

I don’t think mutual funds are bad for everyone. They can still work for people who want a simple, managed option and know they’re paying for that help. For me, the better fit would have been a self-directed account with broad ETFs. That isn’t stock picking or trying to beat the market. It’s about paying less so I can keep more of what the market already gives me. Some people want advice, automatic investing, and fewer decisions. I can understand that if the alternative is not investing at all. A good fund still beats doing nothing.

However, with some education a do-it-yourself approach can be a better strategy. A simple ETF portfolio is often more than enough. By using these funds you can invest in the very same indexes and stocks that mutual fund managers invest in but without high fees. I can’t get those lost years back, and I can’t rewind compounding. But I can stop giving away more than I need to. My next step is simple: review the LIRA, check transfer rules, and compare lower-cost options for future contributions. Even a small cut in fees can help me recover some ground.

My mutual funds didn’t only cost me fees. They cost me market upside, time, and years of compounding that I can’t fully replace. I pay much closer attention now to what I own, what it costs, and whether the convenience is worth the price.

Leave a Reply